What you should know before investing in the podcast industry: A guide to the audio ecosystem.

If you have been following the business news these past two years, you have likely noticed the growing interest in the podcast industry.

Last year, I published an in-depth analysis of the podcast sector to help interested parties understand its history, success, players, and function. Since then, the attention being paid to this marketplace has not faded. If anything, it has only grown bigger. As I am writing this article, SiriusXM has just announced it will be acquiring Sticher for $325 million — the biggest purchase ever made in this sector so far.

But despite many venture investments, IPOs, M&As, new launches, and even a Pulitzer Prize, the industry remains rather small (under the $1 billion mark in the US, as of 2020).

So why does the podcast industry get so much publicity, and should you believe the hype?

I will try to answer these questions while taking a deeper dive into this ecosystem.

What are podcasts, and what is the podcast industry?

A podcast is a professional or nonprofessional, downloadable, audio show, divided into episodes (sometimes seasons) that one can listen to anytime, anywhere, over the internet (regardless of their device). Formats, genres, and production value, vary from one show to another. Most are available on any podcast platform (Apple, Spotify, Stitcher, Himalaya, Luminary…), even if these platforms offer more and more exclusive shows.

Want to read this story later? Save it in Journal.

However, things get complicated when it comes to defining the industry as a whole. Strictly speaking, the podcast industry includes every company producing, hosting, monetizing, or distributing podcasts. However, the “audio industry” appears to be bigger than that, and many companies exist on the edge of what is traditionally called a podcast. For instance, Audible, the biggest platform for audiobook distribution, was acquired by Amazon in 2008 and is now producing original shows and new types of audiobooks that are getting closer to the podcast model. This is also true for meditation apps like Headspace or Calm, as well as educational platforms like Knowable, which are all largely using an audio format. These services are further blurring the definition of podcasts, which is becoming: “anything audio beside music.”

But even with a narrow definition of the industry, the number of investments and exits has recently skyrocketed.

What are the most significant exits and investments:

Podcasting was started by amateurs in the early 2000s and, for the most part, seemed to be largely incompatible with any type of outside investment for a long time. But things have changed dramatically since then, and the coronavirus pandemic has not been an issue for the podcasting sector.

As recently as July of 2020, two major deals have been made. SiriusXM acquired Stitcher, a “full service” podcast company for $325 million, including production, distribution, and advertising. The New York Times bought Serial, a production company, for $25 million. These deals came on the heels of a long list of investments and acquisitions.

I have tried to compile a list of the biggest exits and investments of the past few years below. For clarity, I voluntarily left out some companies that are not strictly doing podcasts, but that are part of this larger ecosystem. As I mentioned, the extend of this industry is not exactly clear. Furthermore, I haven’t included any licensing deals that would be beyond the scope of this section. However, there is at least one that is worth mentioning. In May 2020, Joe Rogan, known to be the most popular podcaster, struck a multi-year licensing agreement with Spotify worth $100 million. His show will eventually become exclusive to the platform but not move (yet!) beyond a paywall.

It is worth noting that venture investments and M&As are growing faster than the overall value of the industry itself. Due to this fact, many believe in the potential of this industry to allow investors to significantly outperform on their investments.

We also noticed a consolidation of the market. Of course, Spotify is trying to become the main (and only) podcast platform, and, until recently, the competition did not seem to react much to its shopping spree. But this is about to change.

SiriusXM has already made two acquisitions. The New York Times has also jumped into the fray as it tries to become the “HBO of podcasts,” according to some analysts. Amazon, Sony, Google, and Apple are testing the waters by mostly developing originals without showing a clear strategy yet. But I predict we will see big acquisitions or projects coming from them in the near future. This is without mentioning the strictly audio companies, such as Luminary and Himalaya, which have invested massively in the industry after receiving $100 million in venture funding each.

So, why is everyone talking about podcasts?

This is where things become truly interesting. As I have mentioned, the market size is not impressive yet. In fact, one can argue that this industry receives a disproportionate level of attention and investment for its size. I personally don’t think so, and I can see five reasons why the podcast industry could interest investors.

Reason #1: Investors look at the key metrics of the industry.

If you have heard of podcasts, it’s probably because you have listened to some yourself. When you think about it, it is pretty amazing to see an emerging industry being so widely and quickly adopted. This is not just an impression. Podcasts are not new but have become widely accessible in the past few years and subsequently have been massively adopted by consumers.

Listenership:

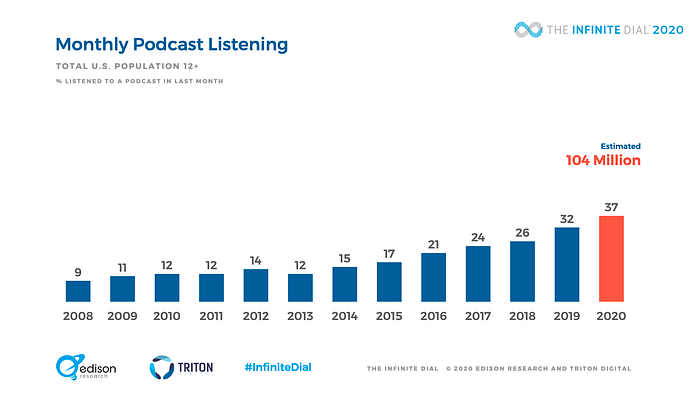

Listenership numbers are impressive. In 2020, 37% of the US population aged 12 and above listened to at least one podcast in the last month. That’s 104 million people! This represents an increase of 17% from 2019 and a doubling since 2015.

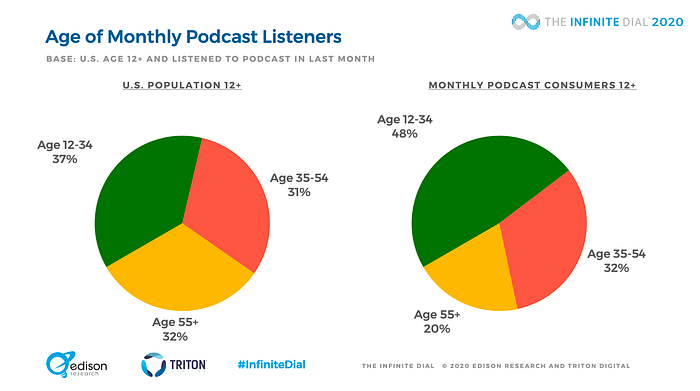

Beyond mere listenership, there are a few other metrics that need to be mentioned in order to grasp the sector’s potential. The average podcast listeners are younger than the consumers of any other medium, but they are also more educated and wealthier than the rest of the population, which promises a likely continuous growth in the future.

The details are also encouraging. Indeed, podcast consumption is not anecdotal. On average, a consumer spends six hours per week listening to nonmusical audio content.

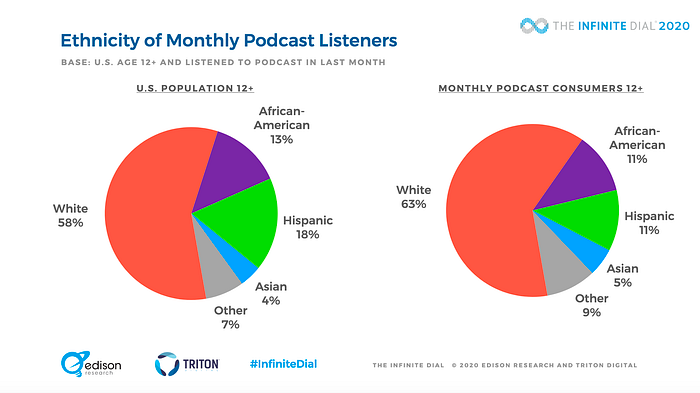

Finally, listeners are diverse and reflect the US population as a whole.

Revenues

Of course, revenues have followed this growth too, but more modestly. While monetization efforts have taken more time than consumer adoption, the sector is still showing high potential for future investors.

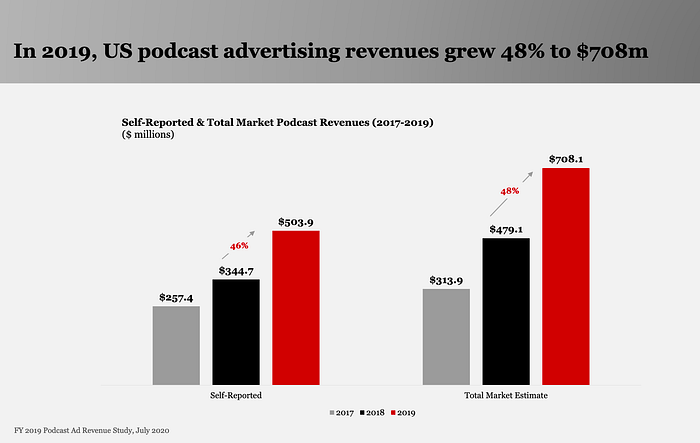

Many believe that the current gap between listenership and market size is going to close within the next few years. Right now, most of the revenues in this industry come from advertisements. If the market is relatively small, it will grow rapidly. Advertisers spent close to $700 million on podcasts in 2019, according to estimates by the IAB and PWC. This represents a 48% increase from 2018, which is higher than what analysts predicted. From what we’ve seen of 2020 so far, this trend is not stopping even with the coronavirus.

Reason #2: Investors look at the ROI of ads.

This could be the most important selling point of all. Podcast ads work very well and are very cheap!

There has been a lot of talk regarding the best way to monetize podcasts, and the industry has a love-hate relationship with advertising. While many industry professionals favor the Netflix business model, it has not proven itself yet. This is still the beginning, and I am convinced some sort of successful audio platforms will emerge, but ads themselves can support the industry’s growth.

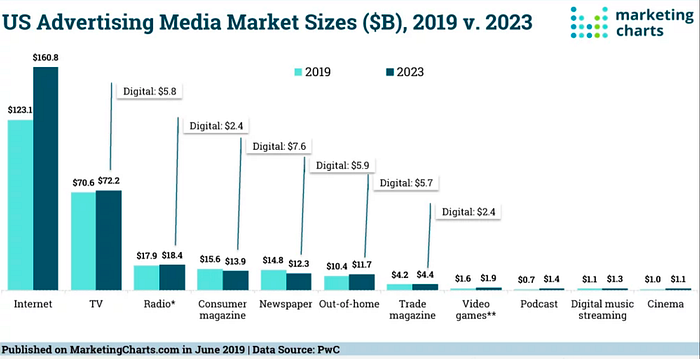

The market size for podcast advertising is expected to double between 2019 to 2023, which constitutes the highest growth for that time period among all forms of media. In comparison, Internet ads will grow by 30%, but most other forms of media will experience slower growth or a decline.

More importantly, the podcast ad market is disproportionately smaller per listener than other forms of media. It is believed that podcasts monetize at only $0.01 per listener hour, which is ten times less than radio and other forms of media.

Moreover, podcast ads are more efficient than ads on other mediums. A study by Nielsen found that pre-roll podcasts ads are more efficient and have a higher conversion rate than pre-roll video ads. Some case studies seem to confirm that podcasts outperform other forms of media.

So why isn’t the industry already bigger? There are many factors explaining the current situation:

· There is a lack of monetization for most podcasts. The minimum number of downloads per podcast needed to enroll in the industry’s ad marketplaces is 50,000, which leaves a substantial part of the industry untapped.

· There is a lack of reliable and consistent measurement standards for specific campaigns.

· The human factor and old habits from marketers also play a role. Podcasts are a relatively new phenomenon, and some advertisers may not want to take a risk.

As the industry matures, ad monetization will become more accessible, metrics will become more detailed and consistent, and marketers will feel more comfortable investing in podcasts.

Spotify already offers tools like “Dynamic Ad Insertion” and signed a deal with Omnicom for $20M to distribute ads for podcasts on its platform for the rest of 2020.

As Conal Byrne, the president of iHeartRadio’s podcasting division, said: “Podcasting has what I genuinely think is the single best ad product in media right now.”

Reason #3: Investors look at what’s happening in China and the rest of the world.

The Chinese podcast market has been perceived as the Holy Grail by the rest of the industry. The total size of the market was close to $8 billion in 2018 (20 times the size of the American market at that time), and many hope that the US will follow.

The success of podcasts (or at least nonmusical audio content) hasn’t appeared to slow down whatsoever. It is expected that the number of users will reach more than 500 million in 2020. And according to iMedia Research, more than 60% of Internet users are willing to pay for audio content.

In China, we also see that listeners are younger and more educated. Almost 90% of podcast listeners are under the age of 35, and slightly more than 86% of them have a bachelor’s degree or higher.

Some studios are now tapping into the Chinese market. For example, Studio Ochenta (based out of Paris) has translated its flagship show “Mija” into Mandarin. In addition to being a potential market opportunity for US companies, the Chinese market shows that a substantial market can be built for audio content and how to build it.

We can also predict that the Indian market will be the next gold mine for the industry and will be more profitable for international companies. If the Chinese market is already mature, the Indian one is still expanding and has not produced any large local audio companies yet. This is why Spotify and Audible have been maneuvering a good bit in India recently.

We have also seen a lot of potential coming from Latin America and Europe, with listeners tuning in more frequently.

To understand the difference in market size, we first need to distinguish between the two main business models that currently exist in the podcast world: the “American” model and the “Chinese” model. The American business model is mostly ad fueled, while the Chinese model is mostly subscription-based. The gap between the revenues from both models is enormous, which is giving ideas to some companies here in America.

Reason #4: Investors look at potential alternative ways of monetizing podcasts.

As of 2020, most podcasts’ revenues come from advertising. But some alternatives are still being tested. As Stitcher CEO, Erik Diehn, said: “We’re all testing out to see what actually sticks. Is it tipping, is it a publisher-by-publisher premium subscriber model, is it the Patreon single-show, single-creator support model, is it a Netflix-type model? There’s not going to be one thing.”

Subscription Business Model:

One option that has been seriously tested for the past year is subscriptions. For now, the results are mixed, but I believe things will change.

Businesses have not yet found the magic formula to attract listeners. In 2019, everyone was talking about building the “Netflix for podcasts,” a paid platform with all the audio on-demand and no ads. This was ignoring the fact that Netflix basically started this business model and had years of quasi-monopoly to become the leader it is now. If five other platforms had started their operations at the same time Netflix went digital, things would have likely turned out differently.

By trying to get every podcast listener on their platforms, these companies have failed (for now) to build a strong and identifiable identity. Currently, they sound more like a paid version of something you can get for free elsewhere.

So, what could change that dynamic? In my opinion, a winning bet will not try to be the Netflix for podcasts, but to aggressively cater to a specific niche. This will attract the most motivated listeners and offer the company a clearly defined brand identity. Finally, the company will need to create some compelling content related to this identity.

For those of you who think that consumers will not pay for audio, you should look at what is happening in China or with the meditation apps that rely on audio and subscriptions. In Europe, one company — Majelan has already shifted its business model from a podcast aggregator startup to offering exclusive content only to paying customers. Wondery has also developed its own app around (mostly) their content, which has a specific brand identity.

One final objection that needs to be addressed is the risk of “subscription fatigue.” This is a real possibility not only for podcasts but also for SVOD services and newsletters. Once again, the solution is to create a clear brand identity by tackling a specific niche, along with great content, therefore avoiding the “Quibi effect,” a technically well-designed product but that nobody wants to pay for.

IP monetization:

Another way to monetize podcasts, which we have seen for at least two years, is through their IP portfolio. Podcasting is a great way to test new projects and see how the market perceives them, since it costs less than developing a film or series.

You may have seen the Oscar-winning movie Whiplash. What you may not know is that, in order to develop the project, a short version of the film was developed first. That was five years ago, and I would bet that today the director would develop a podcast to show the proof of concept rather than a short film. This is what happened to the show “Dear Young Rocker”. After being turned away by TV producers, the writer created a great podcast… which is now being developed for TV.

Some companies have mastered the IP game. Gimlet, for instance, created the show “Homecoming,” which was later developed as a show with Amazon Studios starring Julia Roberts.

Wondery is also great at IP monetization. In early 2020, its COO Jen Sargent confirmed that they had “nine shows in active development, all of which are either optioned or ordered to series across multiple networks and platforms and production houses”, including the infamous Dr. Death (airing later this year on Peacock starring Alec Baldwin).

Finally, other monetization avenues exist that could generate additional revenue, such as the sale of merch or live events (when they resume).

REASONS #5: The market is incredibly resilient.

It would be impossible to discuss any investment without mentioning the coronavirus and its consequences. As we are all navigating through this crisis, investors are scrutinizing the impact of the virus. The entertainment industry has taken a serious hit, especially because of its inability to create new content. But the podcast world has been mostly spared. According to an article published in Digiday in July: “After months of marketplace disruption driven by the coronavirus crisis, the digital advertising market as a whole has no choice but to inch forward unsteadily right now. But for the podcast industry, things are starting to look almost normal.”

At the beginning of the crisis, the industry experienced a small yet substantial drop in listenership. Back in March, people stopped commuting, and podcasting took a big hit, with downloads declining about 10%, according to Chartable.

This could be explained by the fact that listening habits are highly routinized by consumers. Podcast listeners listen mostly while commuting, but also when working out or shopping. However, new routines have emerged and, with them, new listening habits.

The resiliency of this market is excellent news for the industry. It means that consumers are not just consuming podcasts for lack of a better alternative, but because they actually love the content. When habits change, these consumers bring podcasts with them.

Over the past two months (June/July 2020), podcast downloads have returned to their pre-COVID levels. This is also true for ad spending. The space is still expected to grow 15% this year despite the crisis. While this is down from an original projection of 28% growth, it still constitutes a significant increase, especially compared to the complete collapse of the ad market in other sectors. Indeed, podcasts are the only form of media that should see an increase in ad spending.

So, (to conclude), should you believe the hype? The tales of two ecosystems.

I think this presentation shows that a bright future lays ahead for the podcast industry. Everything from customer engagement, to alternative monetization, to advertisement dollars seems to be moving in the same direction: rapid and constant growth for this relatively new medium.

So, should you invest blindly in anything that is remotely related to podcasting?

Of course not. First, there are different types of companies within the podcast industry. Production and monetization companies have been the clear winners so far; however, distribution platforms still need to prove they can attract a substantial base of paying customers.

Second, we need to understand that there are two types of podcast ecosystems competing at the moment. The difference in returns for investors will depend on which system prevails in the end. These two systems are what I call: “the independent ecosystem” and “the companion ecosystem.”

In the “companion ecosystem,” companies are using podcasts as a marketing tool and a means of driving additional traffic toward their main business. So far, this is what Spotify and Apple have been doing.

Originally, Spotify invested in podcasts to retain and attract more paying consumers to its music subscription business, which seems to be working. Customers who are listening to podcasts spend twice as much time on the app as those who don’t. But, in Spotify’s most recently published quarterly financial statements, the company confessed that the many podcast purchases it has made may not “generate sufficient revenue” to “offset the costs of acquiring” them.

Apple is also investing in original podcasts but uses them to promote shows on its streaming service. This is also true for HBO and Netflix. Other production companies and streaming services, like Hulu and Amazon, will inevitably follow.

Conversely, in the “independent ecosystem” scenario, current podcast players, along with newcomers will distinguish themselves from companies whose business model is not audio focused. This is what’s currently happening in China. Luminary, Himalaya, Stitcher, Castbox, and other podcast platforms find their niche and grow to form a rich ecosystem. Podcast production companies will become unicorns and may themselves venture into video, not just the other way around. It is possible to imagine Wondery producing its own true crime documentaries or fictional stories along with its podcasts. Ad networks will also grow, and the now $1 billion dollar market will begin to become comparable to the $18 billion radio ad market.

There is no certitude regarding which scenario will prevail, or if it will be a mix of both, but as stated in a recent study by Deloitte: “The signal is clear: Audiobooks and Podcasts are outgrowing their “niche” status to emerge as substantive markets in their own right.”

If you would like to talk about the Podcast industry or more, you can connect with me via LinkedIn.

📝 Save this story in Journal.

👩💻 Wake up every Sunday morning to the week’s most noteworthy stories in Tech waiting in your inbox. Read the Noteworthy in Tech newsletter.